PwC Whistleblower Alleges Fraud in Audits of Silicon Valley Companies

(Photo: Shutterstock; Illustration by POGO)

This piece is part of a series. See the full series, or skip ahead to the next part, How an Agency You've Never Heard of Is Leaving the Economy at Risk.

After more than a dozen years auditing technology companies in Silicon Valley, Mauro Botta took an extraordinary step: He decided to become a whistleblower.

He drafted an account of what he had seen and experienced as a senior manager at PwC, the accounting firm also known as PricewaterhouseCoopers. Then, in November 2016, he submitted it confidentially to a federal regulator, the Securities and Exchange Commission (SEC).

Under penalty of perjury, Botta described example after example of sloppy if not misleading bookkeeping and weak internal controls at businesses in the Valley.

Botta told the SEC that, when it came to their accounting, companies he observed generally had a “low level of competence.” (He explained to the Project On Government Oversight that he was referring to small and mid-sized companies.)

Auditors like PwC are supposed to serve as independent watchdogs.

But the prime focus of Botta’s whistleblower complaint wasn’t the tech companies. It was something deeper and more far-reaching: the culture of auditing at PwC.

Botta alleged that, to keep corporate managers happy and to avoid losing their business, PwC was pulling its punches—trying not to flag too many problems with companies’ internal controls.

He said he was concerned about “the risk of collusion between auditors and management in this valley . . . with management paying us the fees and auditors picking and choosing what to call an audit issue.”

For instance, he said, one company—whose name is redacted in materials provided to POGO—made a series of mistakes.

First, its controller was duped by an email phishing scam. The controller wired money as directed by a phony email despite the fact that company policy required two signatures for such wire transfers—and despite the fact that the party the controller paid wasn’t on the company’s vendor list.

Second, the company neglected to disclose to the auditors its close relationship with a business “entity” that shared its address and performed research and development at its direction. The entity was not included in the company’s financial statements until auditors raised the issue, he wrote. (Keeping the entity off the company’s books would have reduced the company’s reported expenses, Botta explained to POGO.)

Third, as Botta reported, the company apparently failed to notice that, when it sold a shipment of products, the buyer had a contractual right to return thousands of them. (That could affect the company’s ability to record revenue from the sale, Botta clarified for POGO.)

PwC was pulling its punches—trying not to flag too many problems with companies’ internal controls, Botta alleged.

Those were just some of the company’s alleged problems.

Botta told the SEC that he proposed stating in PwC’s audit report that the company had “a material weakness” in “the skill and competence of the finance department.” Botta wrote that, in response, he “was put under significant pressure” by superiors at PwC and was told that if he pursued that path, it was unlikely he would be promoted to partner.

Then, the chief financial officer of the company PwC was auditing asked PwC to remove Botta from the audit—and PwC agreed, Botta wrote.

“The firm accepted to remove me ignoring my claim that the competence of management would still constitute a significant risk,” Botta wrote.

The PwC veteran isn’t alleging that a bunch of technology companies are reporting false profits. Rather, he’s alleging that in many instances the numbers companies report are correct only because the outside auditors corrected them.

He argues that members of the public—including the shareholders who pay corporate executives—are entitled to that information, and he asserts that auditors have breached their duty by withholding it.

In a recently filed lawsuit, Botta alleges that PwC fired him in retaliation for standing up to “fraudulent,” “deceptive,” and “negligent” practices at the accounting firm and for reporting that conduct to the SEC.

If Botta’s take on auditing in Silicon Valley is on the mark, it’s another in a history of reasons to doubt the auditors and the federal system charged with protecting investors. And it comes at a time when the Trump Administration is positioned to put its imprint on the obscure organization that regulates audit firms like PwC.

Douglas R. Carmichael, an accounting professor and former auditing regulator, told POGO that the picture Botta presented is “very disturbing.”

In response to questions from POGO, PwC spokeswoman Sarah Tropiano provided a brief statement:

“The claims presented in the lawsuit are false. PwC maintains the highest ethical standards around our business and a robust code of conduct that protects whistleblowers. Mr. Botta’s employment was terminated for legitimate business reasons, and we will demonstrate that in court.”

“We decline to comment further at this point as we will litigate the matter in court,” Tropiano wrote.

Douglas R. Carmichael, an accounting professor and former auditing regulator, told POGO that the picture Botta presented is “very disturbing.”

If the facts are as alleged, Carmichael said, “I think it undermines the confidence in audit reports.”

The Watchdog’s Duty

Auditors like PwC are supposed to serve as independent watchdogs. Investors, lenders and others rely on their work when putting money at risk—including, for instance, pension and retirement funds.

“This ‘public watchdog’ function demands that the accountant maintain total independence from the client at all times, and requires complete fidelity to the public trust,” the U.S. Supreme Court stated in a 1984 decision.

Since the 1930s, the government has required publicly traded companies to obtain outside audits, which means the accounting firms that fill that role profit from a federally mandated franchise.

In addition to scrutinizing companies’ finances, auditors are now responsible for reporting on companies’ internal controls. Those can include accounting processes, information technology systems, and other checks and balances that guard against fraud and potentially affect the reliability of corporate financial statements.

The government required auditors to report on internal controls under the Sarbanes-Oxley Act of 2002, which was written in response to a wave of accounting scandals. Companies such as Enron and WorldCom had used accounting tricks to obscure their true financial condition, and auditors had failed to sound an alarm. When the truth emerged, the companies imploded, investors lost many billions of dollars, and workers’ jobs evaporated.

The new auditing requirement generated more work—and more fees—for audit firms. In return, the public is supposed to be getting valuable information. The auditors’ reports on internal controls can shed light on the character and competence of management and a company’s vulnerability to financial fraud or error.

But Botta’s story helps to illuminate a fundamental problem that the government has long condoned: Far from being independent, accounting firms are hired and paid by the companies they audit. That gives them powerful incentives to curry favor with the very corporate managers they have a duty to oversee.

In his complaint to the SEC and in his lawsuit, Botta alleged that a PwC partner advised him to let problems slide. The partner allegedly said that many Silicon Valley companies had material weaknesses, but if PwC cited them all, it wouldn’t be able to compete with other audit firms.

The trust and responsibility that the government vests in audit firms assumes they will bite the hand that feeds them, and biting is not necessarily the best business model. It should come as no surprise if audit firms are interested in ingratiating themselves to their clients.

Time and again, from the savings and loan crisis to the dotcom bubble, from Enron and WorldCom to the mortgage meltdown, the financial crisis, and countless other corporate scandals, accounting watchdogs helped lull the public into a false sense of security.

Botta’s SEC filing warned of trouble in the heart of the information economy, the valley that symbolizes American innovation.

Behind the Veil

Though auditing’s built-in conflicts of interest may be obvious, they are seldom shown as clearly as in an internal PwC document Botta shared with the Project On Government Oversight. The document, dated May 2014, gave Botta feedback on his performance. It compiled comments from several PwC partners the firm had surveyed, showing in their anonymous words what it takes to become a PwC partner and how they expected PwC auditors to deal with clients.

The feedback included comments such as these:

“Build the relationships where the client would never want to leave PwC.”

“As a partner you have to have the position that you want these guys to like you . . . .”

“If he were really responsible for bringing in the revenue and keeping clients, as partners are, he would have to adapt fast.”

The May 2014 feedback survey suggested that the auditor needed the support of audit clients to advance at PwC.

“Until he gets the clients pounding the table for him, I don’t think he’ll ever make partner,” the survey said.

Under auditing rules, auditors are not supposed to do the accounting for their clients. That would amount to auditing their own work. Their job is to opine on the client’s work.

However, in his complaint to the SEC, Botta said that PwC frequently ends up doing clients’ work for them and fixing problems rather than disclosing them. He said that, to compensate for technology companies’ accounting weakness, auditors had assumed the role of advisors to management. Botta wrote that, at a PwC training session on documenting certain controls, a PwC sector leader said “we know that factually we have to manufacture most of the documentation because client [sic] don’t have it or don’t know how to do it or don’t want to spend the money to do it.”

The May 2014 feedback survey made similar points.

“[B]ecome a trusted advisor to the client,” the survey advised.

“When you get to be a partner they need someone to confide in and trust who will look out for you.”

In the survey, one partner recounted an episode in which Botta refused to prop up a client.

“Our client asked for help to do a write up,” the partner recounted. “A Partner would just get to work and write the memo and figure out how to conclude our opinion. Mauro would not give them the memo. His position was that it is not our responsibility to do that.”

(Botta told POGO the “write up” in question was apparently a technical memo the client was required to produce to support the way it accounted for a complex financial instrument.)

Auditors are supposed to be skeptical, and audits are supposed to be based on verification rather than trust. The May 2014 survey offered this feedback on Botta’s mindset and approach:

“I don’t think the way he develops his client relationships is very effective. He doesn’t trust any of his clients.”

“His core personality is being a really good auditor, but that doesn’t mean you can be a really good partner.”

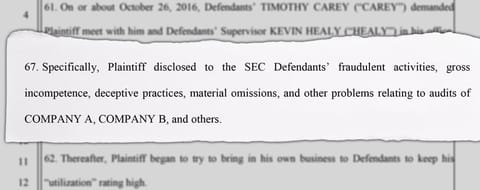

In his complaint to the SEC, Botta said PwC had created an environment in which it was not safe to speak up. In the feedback survey, alluding to the highest score an employee could earn on a performance review, partners’ comments included the following:

“When you are a 1 rated top performer/partner, you tow the party line.”

“An emotional Italian guy”

Botta, 40, grew up in Italy, joined PwC there in 1999, and transferred to the firm’s San Jose office—which serves Silicon Valley—in 2004.

English is a second language for him, and he speaks with a pronounced accent.

In 2013, a PwC newsletter in Italy featured an autobiographical article by Botta describing his journey to America and his experience living and working in San Jose.

"Il Volo," a PwC Italy newsletter, featured Mauro Botta in 2013. (Source: Il Volo)

“American culture, which may appear free, is in reality a bit repressed when you talk about work environment,” Botta wrote, according to his own translation of the Italian. “Swamped with attorneys which sue for anything, American culture adapted itself into a sort of self-censorship which leads people in public not to talk about controversial topics,” he added. “Speaking for myself, I am still living the American dream of individual freedom and this has led me to challenge a lot of taboos, starting from talking about any topic in public, to always voice my opinion in any possible occasion.”

The May 2014 feedback survey described him as “quirky,” noting his interest in Star Trek conventions, and it advised him to “keep it culturally appropriate.”

Botta told the Project On Government Oversight that he’s interested in Star Trek the way some people are interested in golf, and he said he has worn a Star Trek outfit to work on weekends to boost morale.

In answer to the question “What is preventing Mauro from being rated a top performer and/or progressing to partner?” the feedback survey described him as “an emotional Italian guy,” a comment he has cited as evidence of ethnic bias.

Mauro Botta takes an Oath of Allegiance during his naturalization ceremony to become a US citizen in 2011. (Photo courtesy of Mauro Botta)

But that was not the persona on display in telephone interviews or after he took a red-eye flight to Washington to meet with POGO one Saturday in April. Instead, he came across as methodical, firm in his professional convictions, and detail-oriented—consistent with other observations in the feedback survey.

Since early April, Botta has participated in a series of interviews with POGO. He also provided copies of various documents, including the feedback survey and his complaint to the SEC. He did so on condition that the material not be published until he had filed the lawsuit he was preparing against PwC. To protect client confidentiality, Botta redacted company names and the dollar amounts associated with accounting issues. He also redacted the names of PwC personnel, though some of them are named in his lawsuit.

People who submit tips and complaints to the SEC may be eligible for whistleblower rewards if their information leads to SEC enforcement actions.

The fact that Botta has not disclosed the names of the audit clients he described in his SEC complaint and lawsuit limits POGO’s ability to investigate his allegations.

However, the May 2014 feedback survey shows PwC partners speaking in their own words.

The document’s overall assessment of Botta was glowing.

“[Y]ou are widely respected and thought of as a tremendous asset to PwC,” the introduction said.

Other comments backed that up.

“Dedicated, loyal, hard working.”

“Strong set of values, high integrity, trust worthy, ability to call a spade a spade.”

“Mauro has a very strong professional skepticism and it is a very good thing.”

There was also this:

“He tends to be too black and white.”

“[H]e does not have a filter.”

“He throws partners under the bus.”

On a scale of 1 to 5, where 1 was the top rating, Botta received a rating of 1 for 2014 and 2015, he said. In time, as his standing at the firm declined, his rating fell to a 3, he said.

By his own account, he pressed disagreements with partners when he thought they were acting incorrectly, was cautioned that he was jeopardizing his career, and repeatedly resigned from the firm only to be talked into staying. Also by his own account, he was repeatedly taken off audits at the request of companies PwC was auditing.

Increasingly, he said, he found himself sidelined.

A Professor’s Perspective

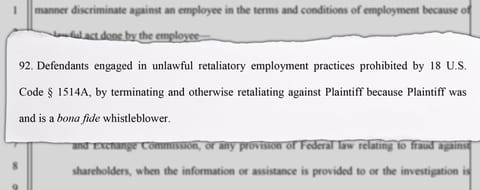

Carmichael, a professor at the City University of New York’s Baruch College, reviewed documents cited in this report at POGO’s request. Carmichael has served as chief auditor at the Public Company Accounting Oversight Board (PCAOB), a regulatory body created in the aftermath of the Enron and WorldCom scandals to oversee corporate auditors. Earlier in his career, he was vice president for auditing at the American Institute of Certified Public Accountants, a professional organization. Carmichael noted that he has testified as an expert witness against PwC.

Carmichael said some of the conduct Botta described would be “just terrible.”

The professor said he was especially troubled by the notion that PwC would let matters slide to remain competitive with other audit firms.

“That’s the attitude that can result in a race to the bottom,” he said.

In the feedback survey, “they seem to be saying he’s not partner material because he’s too aggressive about adhering to the standards,” Carmichael said. “Certainly there are a good many of them that seem to be saying . . . ‘We have to be willing to look the other way.’”

Carmichael said he was also troubled by an alleged effort to mislead inspectors from the oversight board. In his complaint to the SEC, Botta said priorities at the audit firm’s Silicon Valley office included “profitability or selling additional services,” a reference to selling PwC consulting services to companies the firm audits. Botta alleged that PwC partners told him they had been cautioned not to put those priorities in written plans to avoid raising questions from the regulators.

“That’s very disturbing,” Carmichael said.

Carmichael agreed that some of the problems Botta cited at companies PwC audited would rise to the level of material weaknesses warranting disclosure in audit reports.

Botta’s narrative reminded Carmichael of an earlier era.

“That just goes back to a time in the 1970s, I would say, where auditors were allowing accounting that was clearly in violation of standards just because other firms had permitted the accounting and they couldn’t be competitive any more if they insisted on the right accounting.”

It also suggested a reversal of progress made since the creation of the oversight board, Carmichael said.

“If it’s reflective of [a] firm-wide attitude and not an aberration of a particular office, it could seriously undermine the confidence that has been built up over that fifteen year period.”

Lynn Turner, a former chief accountant at the SEC and former technology executive, said he witnessed a race-to-the-bottom dynamic in the 1990s when he was in charge of the nationwide high-tech audit practice at Coopers & Lybrand, one of the firms that merged to form PwC. Turner said accounting firms “jumped in the gutter together” and vied to be lenient with companies they audited.

“They didn’t want to have a reputation amongst the venture capitalists”—who could influence the selection of auditors—“that they were a really diligent, tough auditor,” Turner said.

“Recurring Audit Deficiencies”

Botta’s accusations add to a broader picture.

In November 2017, the PCAOB warned about the “number and significance of the recurring audit deficiencies” identified in its inspections.

“Deficiencies in audits of internal control over financial reporting continued to be the most frequent deficiencies identified by PCAOB inspectors in 2016, consistent with prior years' results,” the auditing oversight board added.

PwC might be most famous lately for flubbing its role at the 2017 Academy Awards, but little-noticed reviews by that obscure regulator tell a more consequential story.

In a December 2017 report on its 2016 inspection of PricewaterhouseCoopers LLP, the oversight board said it looked at 56 PwC audit engagements and discovered deficiencies so serious that it appeared the favorable opinions PwC issued in 11 of those audits were unfounded.

Meanwhile, former oversight board employees and leaders of accounting firm KPMG stand accused of engaging in a criminal conspiracy. After KPMG fared poorly in oversight board inspections, it recruited employees from the board and then used them to get confidential information on which audits the board was planning to inspect, the Justice Department alleged in January 2018.

If the charges in the indictment are true, key personnel at one of the world’s biggest accounting firms had corrupted the system meant to make accountants more accountable.

Some of the key players in the system today are themselves veterans of the accounting industry.

In December 2017, the SEC appointed a completely new slate of leaders to the oversight board. One of the five new board members, James G. Kaiser, joined the board from PwC, where he was responsible for “innovation in auditing,” the SEC said. Kaiser had been with PwC for 38 years.

Many expect the oversight board’s new leadership to take a much more hands-off approach to regulating auditing firms following showdowns over the last board chairman’s efforts to strengthen accountability rules. “Obviously there has been some tension that has built up over the years, particularly between the firms, the business lobby and the board,” Michael Shaub, an accounting professor at Texas A&M University, told The Wall Street Journal after the SEC made the appointments. “It looks like they are reconstituting it. It’s literally a reset.”

In the news release announcing the appointments, SEC Chief Accountant Wesley Bricker pronounced the new members “well qualified to lead the PCAOB.”

Bricker, too, personifies the close ties between the accounting industry and its overseers. According to an official bio, he joined the SEC from PricewaterhouseCoopers LLP.

Damages

A recent federal court ruling against PwC delivered a reminder of why audits matter.

Year after year, from 2002 through 2008, PwC issued so-called “clean” audit opinions on The Colonial BancGroup Inc., parent of Colonial Bank, which was one of the largest banks in the United States. Then, in 2009, amid the wider financial crisis, FBI agents raided Colonial, state regulators closed it, the FDIC stepped in, and the company sought bankruptcy protection.

The bank had been the victim of a long-running multi-billion dollar fraud, and PwC had missed it, the court recounted. A federal judge declared in December 2017 that the audit firm had been negligent.

The FDIC has asked the court to order PwC to pay damages of $625.3 million. PwC has argued that the FDIC is entitled to less than half that amount: $306.7 million.

In a February 2018 settlement with the Justice Department for allegedly failed audits of another company involved in the same fraud, auditor Deloitte & Touche agreed to pay $149.5 million. In a statement provided by Deloitte spokesman Jonathan Gandal, the firm defended its performance. “Deloitte & Touche is deeply committed to the highest standards of professionalism, and we stand behind this work that dates back over a decade,” the firm said.

Turner, the former chief accountant at the SEC, told POGO that, for a while, it appeared that auditing had improved. The scandals at companies such as Enron and WorldCom and the demise of their audit firm, Arthur Andersen, “shook a lot of people up,” Turner said. But, as Turner sees it, the effect has been wearing off, and the quality of auditing “has slipped back . . . even to the point of where we were before.”

PwC’s recent difficulties stretch all the way to India, where, amid the fallout from a major accounting fraud, the audit firm’s Indian affiliate in January 2018 was prohibited from auditing listed companies for two years.

Responding to the ban, the PwC India firm said there was “no intentional wrongdoing by PW firms” in the fraud, which took place almost a decade ago at a company called Satyam. “We have however learnt the lessons of Satyam and invested heavily over the last nine years in building a robust and high quality audit practice,” the firm added—apparently implying that it did not have a robust and high quality audit practice before the fraud.

PwC’s recent problems also extend to Silicon Valley-based Facebook. In its role as a monitor for the Federal Trade Commission, The New York Times reported, PwC effectively gave Facebook’s privacy protections a clean bill of health.

PwC effectively gave Facebook’s privacy protections a clean bill of health.

“In our opinion, Facebook’s privacy controls were operating with sufficient effectiveness to provide reasonable assurance to protect the privacy of covered information,” PwC said in its assessment, which covered the two-year period ending February 11, 2017.

During that period, the Times reported, “Facebook was aware that a researcher based in Britain, Aleksandr Kogan, had provided Cambridge Analytica with private Facebook data from millions of users. Cambridge Analytica, which later worked for the Trump campaign, used the information to build psychological profiles of American voters before the 2016 election.”

Hitching a Ride

In 2017, after he filed his whistleblower complaint against PwC, Botta had a series of calls and meetings with officials from the SEC.

As Botta recounted, one official zeroed in on a scene Botta described in the complaint—an episode that, as Botta saw it, seemed to symbolize a breakdown of auditor independence.

During a PwC meeting in early 2016, Botta had written, staff members were shown a slide of a PwC audit team in front of a private jet. It was the aircraft of the CEO of a company PwC was auditing.

According to Botta, a PwC senior manager explained that when the flight the auditors were supposed to take was cancelled, the CEO “took the whole team on his private jet” and flew them to the San Jose area so they could make it to a PwC party.

According to Botta, the PwC senior manager displaying the picture presented it as an illustration of best practices—showing that the auditors had a great relationship with their client.

One PwC partner who witnessed that presentation was “clearly unhappy about it,” Botta added.

It appeared Botta had gotten the SEC’s attention. In an email dated February 22, 2017, a senior attorney in the SEC’s Division of Enforcement thanked Botta for his time that day. The email suggested the SEC had opened a file; the subject line read, “In the Matter of PricewaterhouseCoopers Auditor Independence Inquiry (NY-09482).”

Escorted from the Building

In the weeks that followed, Botta learned from PwC that that the SEC was looking into PwC’s auditing of one of the companies named in his whistleblower complaint, Botta’s lawsuit says.

PwC opened an internal probe and questioned Botta repeatedly, he said.

In June 2017, PwC supervisors told Botta that, as a result of a restructuring at the firm, he should look for a new job, the lawsuit says. Then, in August 2017, Botta was summoned to a meeting at which PwC Vice Chairman Kevin Baldwin and a human resources leader fired him, the lawsuit says. Botta was immediately escorted from the building, the suit says.

Botta told POGO that he was accused of falsifying work papers.

According to his lawsuit, PwC knew Botta was the whistleblower and gave a false reason for firing him.

SEC enforcement lawyers who communicated with Botta about his complaint referred POGO to the SEC’s press office, where agency spokesman John Nester declined to comment. The SEC generally refrains from commenting on whether it has opened an investigation or on the status of its investigations, the agency’s website explains.

However, in February 2018, Botta said, his attorney got a call from the whistleblower office at the SEC. The SEC official said the agency would not be pursuing an enforcement action against PwC.

Botta said he is awaiting written confirmation of that decision.

Related Content