The Incredibly Shrinking Defense Industry

U.S. Marines aboard amphibious assault ship USS Boxer (LHD 4) conduct post-flight checks on an AV-8B Harrier II attached to Marine Medium Tiltrotor Squadron (VMM) 163 during flight operations on the flight deck in the Pacific Ocean, May 26, 2019. (Photo: U.S. Navy / Mass Communication Specialist 3rd Class Alexander C. Kubitza)

When I began covering the U.S. military for the Fort Worth Star-Telegram in Washington 40 years ago, it was to report on the Texas contractors who built what the Pentagon bought. Tens of thousands of the paper’s readers cared a lot about the fate of the weapons rolling off their assembly lines. Cuts in production ordered by the Pentagon or Congress in faraway Washington could take food off their table; boosts could lead to overtime on the line and a fatter paycheck.

The “military-industrial complex” that President (and five-star Army general) Dwight Eisenhower warned us of in 1961 has funneled down to a few “Walmarts of war.”

Back then, General Dynamics was building the Air Force’s agile F-16 fighter on Fort Worth’s west side. Vought was building the Navy’s A-7 attack plane nearby. And Texas Instruments (TI) was building the revolutionary High-Speed Anti-Radiation Missile—HARM—which could destroy enemy radars. But as the U.S. defense industry entered a post-Cold War contraction, a rash of mergers changed all those name plates. The F-16 ended up being built by Lockheed Martin. Vought was spun off from the LTV Corp., a once-powerful conglomerate, with pieces ending up in the arms of Northrop Grumman. And the HARM missile is no longer produced by TI, but by the Raytheon Corp.

The merger mania that surged as the Cold War wound down—when 51 aerospace and defense companies shrank to five—is making a comeback. The “military-industrial complex” that President (and five-star Army general) Dwight Eisenhower warned us of in 1961 has funneled down to a few “Walmarts of war,” as Daniel Wirls, a professor at the University of California, Santa Cruz, quoted defense researchers calling the surviving contractors in a June 26 Washington Post column. Less competition can drive up costs while dampening innovation. Backers counter that efficiencies, job cuts, primarily, lead to lower costs that can save the Pentagon money—rarely—or let it buy more for the same price—also rare. And the middlemen—the lawyers and financiers who nurture these deals—do just fine, thanks.

Mergers’ merits are murky when it comes to costs and innovation, and haven’t been studied much. It’d be a good move, both for taxpayers and the government, if Congress and the Government Accountability Office took deep dives into the issue to learn enough to make smart decisions. The issue has been debated for decades. Back in 1997, Robert Pitofsky, former chairman of the Federal Trade Commission (FTC), told Congress that the FTC “strongly believes … that competition produces the best goods at the lowest prices and is also most conducive to innovation.”

The latest chapter in Pentagon-contractor consolidation is the June 9 announcement that Raytheon and the defense division of United Technologies Corp. plan to merge. And this announcement comes four years after United Technologies sold its Sikorsky helicopter unit to Lockheed Martin, the Pentagon’s biggest contractor, for $9 billion. The pending merger includes United Technologies’ booming aerospace business—jet engines (including those for the F-35, as well as the F-15, F-16, and F-22) and cockpit electronics—with Raytheon, builder of Tomahawk cruise missiles (acquired when it bought Hughes Aircraft in 1997, which acquired it when it purchased General Dynamics’ missile division in 1992) and ground-fired Patriot air-defense missile systems. The new company—to be known as Raytheon Technologies—would have annual sales of about $74 billion. The companies have set up a website to herald their union.

The Raytheon-United Technologies deal is just the latest in a series of mergers in the defense industry: Over the past year, United Technologies bought Rockwell Collins for $30 billion, defense companies Harris Corp. and L3 Technologies agreed to merge in a $34 billion deal, and Northrop bought rocket-maker Orbital ATK for $9.2 billion.

The Raytheon-United Technologies combo boasts 60,000 engineers and 38,000 patents. Both are generally “platform agnostic,” building pieces for aircraft, tanks, and ships built by others, and they rarely compete with one another for Pentagon contracts. That suggests the federal government won’t object to the deal, which is expected to close in the first half of 2020.

A report from the Trump Administration said the nation has an increasingly “fragile” defense-industrial base with “entire industries near domestic extinction” and growing reliance on foreign sources.

The Justice Department is the federal agency that reviews such mergers, with input from both the Pentagon and the Federal Trade Commission. The Pentagon’s Office of Industrial Policy is primarily focused on the national security impact of such consolidations that might reduce military might, while Justice and the FTC are more concerned with broader antitrust issues that could lead to military-hardware monopolies. Although the Obama Administration’s policy was that it would oppose mergers among the Big 5 defense firms, the Trump Administration hasn’t endorsed that view. (The five contractors doing the most business with the Pentagon in 2018 were Lockheed in the top spot, followed by Raytheon, BAE Systems, Northrop Grumman, and Boeing; United Technologies ranked 11th).

Still, the commander in chief is fretting about this merger nonetheless. “I am a little concerned about United Technologies and Raytheon because one of the things that I bring up all of the time, we used to have many plane companies,” President Trump told CNBC shortly after the companies announced their plan to join forces. “We used to have many, many. They’ve all merged. Now we have very few. … It is hard to negotiate when you have two companies and sometimes you get one bid.”

(Source: GAO-19-336SP, page 3)

The pending Raytheon-United Technologies deal “would fall just below the previous policy’s formal redline but gets about as close to that line as possible,” an analysis of the proposed merger by the nonprofit Center for Strategic and International Studies said. While the Center said government approval is expected, “it is almost inevitable that the new company will be required to divest some defense capabilities, and potentially some commercial ones, that overlap between Raytheon and United Technologies to preserve competition.”

Defense mergers have accelerated recently, in part because of “early guidance from the new U.S. administration” that defense spending would be on the rise, consulting firm Deloitte said in a 2017 report. In fact, 80 percent of professionals in the aerospace, defense, and government services sectors are bullish on mergers. That’s according to a survey released in April by the independent investment banking firm KippsDeSanto in the heart of suburban Virginia’s defense-contracting nirvana. “We have been in a really good budgetary environment,” Managing Director Michael Misantone told National Defense in April, citing a “large increase in defense spending” as rocket fuel for military mergers.

Between 2008 and 2018, the average cost of a Pentagon weapons system—not including inflation—jumped by 13 percent, the Government Accountability Office said.

Of course, it was only a generation ago that precisely the opposite was true. It was plummeting defense budgets that were making mergers all but inevitable—under orders from the Pentagon itself. Then-Defense Secretary Les Aspin and his deputy, Bill Perry, invited the top officials from the nation’s biggest contractors to a dinner at the Pentagon in 1993 to warn that they all wouldn’t survive the coming budget crunch. “We expect defense companies to go out of business,” Perry, who succeeded Aspin as defense secretary in 1994, said after what came to be called “the Last Supper” in defense-contracting circles. “We will stand by and watch it happen.”

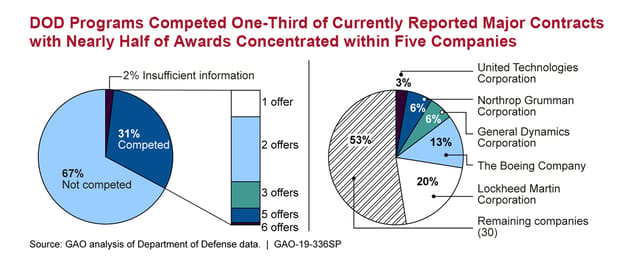

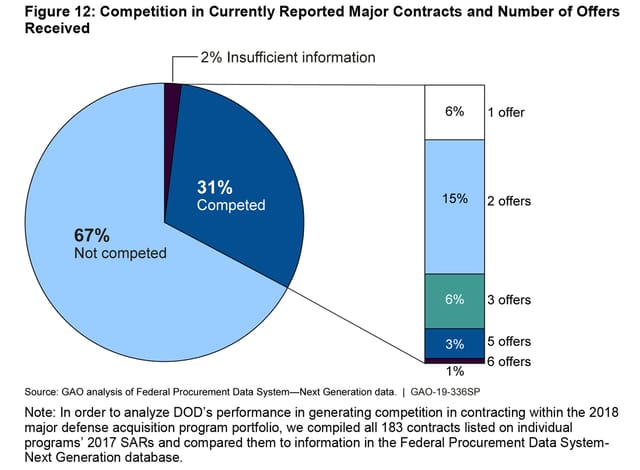

In May, the Government Accountability Office (GAO) noted the dire effect of consolidation. Even though the Pentagon has cut four programs from its must-have list, the GAO said, its remaining 82 major programs had grown in cost by $8 billion, to a cool $1.69 trillion. “Portfolio-wide cost growth has occurred in an environment where awards are often made without full and open competition,” the Congressional watchdog agency added. “Specifically, GAO found that DOD did not compete 67 percent of 183 major contracts currently reported for its 82 major programs.” Nearly half of those contracts—47 percent—went the current Big 5: Lockheed, Boeing, General Dynamics, Northrop, and United Technologies (the numbers are even grimmer for taxpayers if supposedly “competitive” bids lead to only a single bidder).

(Source: GAO-19-336SP, page 37)

Between 2008 and 2018, the average cost of a Pentagon weapons system—not including inflation—jumped by 13 percent, the report said. “We have reported that competition is the cornerstone of a sound acquisition process and a critical tool for achieving the best return on investment for taxpayers,” the GAO added. “Generally, a low competition rate can contribute to increased costs of goods and services and decreased buying power.”

We’ve heard similar refrains before. Then-Defense Secretary Ashton Carter said in 2015 that he worried about reaching a point “where we did not have multiple vendors who could compete with one another on many programs.”

The health of the defense-industrial base has been a perennial concern. The latest warning about the Pentagon’s shriveling supplier corps was issued by the Defense Department’s own Office of Manufacturing and Industrial Base Policy on May 13. While big defense-contractor profits remain juicy, many smaller Pentagon suppliers are struggling. And the number of contractors doing defense work is shrinking: 97 percent of the Pentagon’s missiles are built by Lockheed and Raytheon. And 98 percent of the lower-level subcontractors making parts for U.S. munitions are the only source for the military parts they make.

Worse, the Pentagon pipeline for missiles and munitions is plagued with problems, including “material obsolescence and lack of redundant capability, lack of visibility into sub-tier suppliers causing delays in the notification of issues, loss of design and production skill, production gaps and lack of surge capacity planning, and aging infrastructure to manufacture and test the products,” the report warns. “Production gaps for munitions and missiles directly reduce the U.S. capability to deliver kinetic effects against adversaries.” In October, a second report from the Trump Administration said the nation has an increasingly “fragile” defense-industrial base with “entire industries near domestic extinction” and growing reliance on foreign sources.

“There are currently only two domestic suppliers for solid rocket motors used in the majority of DoD missile systems, with a single foreign supplier making up the balance,” the report said. More than 80 percent of the Pentagon’s armored vehicles are built by a single manufacturer in a single plant. There is only a single company producing chaff, the foil-like fibers U.S. warplanes eject to distract incoming missiles.

(Source: National Bureau of Economic Research, page 44)

And don’t count on mergers to spur innovation. Innovation requires the levers of competition to work. Competition drives the perpetual quest to get more bang for the buck by harnessing new technologies. The Pentagon acknowledged as much in 1998 when it succeeded in stopping Lockheed’s move to buy Northrop Grumman. But the shrinking number of contractors is leading to less competition, and therefore less innovation.

“Any shrinking in the number of these enterprises ought to be a matter of concern for the defense agencies and for government antitrust agencies,” William Kovacic, a professor at George Washington University Law School and former head of the Federal Trade Commission, said in the wake of the Raytheon-UTC announcement.

This merger trend isn’t likely to end well, at least for U.S. taxpayers and the military they support. “If the trend to smaller and smaller numbers of weapon system prime contractors continues, one can foresee a future in which the department has at most two or three very large suppliers for all the major weapons systems that we acquire,” Frank Kendall said in 2015, while serving as the undersecretary of defense for acquisition, technology and logistics. “The Department would not consider this to be a positive development, and the American public should not either.”