The Great Pandemic Swindle: Feds Botched Review of Billions in Suspect PPP Loans

(Photos: Getty Images; Photo Illustration: Leslie Garvey / POGO)

The Small Business Administration (SBA) flagged nearly 2.3 million Paycheck Protection Program (PPP) loans worth at least $189 billion — about a quarter of the roughly $800 billion lent out — for further review between August 2020 and September 2021, according to a massive dataset obtained by the Project On Government Oversight (POGO) through a Freedom of Information Act lawsuit. There are 4.3 million flags signifying concerns that loans were potentially fraudulent, the recipient was possibly ineligible, or the loans in question merited closer examination for some other reason. There is an average of 1.9 flags for each of the loans identified for scrutiny.

The SBA has forgiven 95% of all PPP loan dollars as of this month. That means a substantial number of loans flagged as potentially going to fraudsters or ineligible recipients have now been forgiven.

Get the latest

Weekly newsletter and occasional updates

The agency first began retrospectively applying these flags in 2020 to help identify loans that should be more closely assessed before being forgiven. Indeed, the SBA dubbed the flags “hold codes,” and the codes were supposed to be cleared before the agency forgave the loans. Yet previously unreported auditor findings state that the SBA failed to ensure that all flagged loans and forgiveness applications were properly reviewed, raising the possibility that the government wrongly waived the repayment of tens of billions of dollars in PPP loans.

The data obtained by POGO appears to show mass close-outs of 2.7 million flags on two separate days near the end of the Trump administration. On a third day shortly before President Joe Biden’s inauguration, the SBA cleared out 99.1% of “special review” flags, almost entirely assigned to the very largest PPP loans above $2 million.

The SBA has made changes to allow it to examine forgiven loans. However, the SBA’s inspector general warned earlier this year that oversight failures both on the front end when the loans were approved and on the back end when they were forgiven may make it challenging “to recover funds for forgiven loans later determined to be ineligible.”

The issuance of the first flags four months after the program began on April 3, 2020, according to the government data, also lends further support to criticism by the agency’s inspector general and other watchdog officials that SBA did not put basic guardrails in place early in the program, which stopped issuing loans on May 31, 2021.

Government estimates of PPP fraud run as high as $100 billion.

The data obtained by POGO appears to show mass close-outs of 2.7 million flags on two separate days near the end of the Trump administration.

Regarding the auditor's findings and SBA's bulk close-outs of flags taken in the last months under President Donald Trump, an SBA spokesperson told POGO that “SBA cannot comment on past Trump Administration decisions.”

But the spokesperson said that prior to 2020's COVID relief programs, such as PPP, “SBA had a solid record” of audits regarding the agency's financial statements “with no material weakness in internal controls and no findings related to fraud risk management.”

“Under the Biden-Harris Administration, SBA’s loan review process adheres to the published rules for the program,” the spokesperson wrote. “From Day One, it has been a priority to address issues inherited from decision makers in the Trump Administration.”

These new revelations that many flags were not sufficiently reviewed may draw further scrutiny to the high rate of PPP loan forgiveness. PPP forgiveness recently garnered renewed attention amid a public debate over the Biden White House’s executive order to forgive a limited amount of outstanding student loans for qualified borrowers who make under $125,000 a year. POGO’s investigation also comes weeks after the Justice Department charged 47 individuals for defrauding the government of $250 million intended for feeding impoverished children — the biggest pandemic fraud case brought to date.

A De Facto Honor System

These flagged loans were not always adequately scrutinized, according to an auditor’s report. Last fall, the auditor found that SBA failed to ensure loans were “completely and accurately reviewed to address their respective eligibility flags.”

There was a rush to close out flags. In late 2020, the SBA had a contractor develop a “tool to expedite the manual review process” by grouping flagged loans in bulk as requiring “no further action,” according to the Pandemic Response Accountability Committee. The auditor’s report found that the SBA trusted — without checking — a key contractor’s review of the flagged loans and didn’t examine the loans the contractor determined were fine. (A new auditor’s report is anticipated later this year, a spokesperson for the SBA’s inspector general told POGO.)

Compounding the oversight shortfalls, “only a limited number of PPP forgiveness applications were actually reviewed” by the SBA, according to the auditor, and “$49 billion was paid to lenders for forgiveness of PPP loan guarantees that were still being reviewed to address alerts and flags indicative of eligibility concerns.” The SBA disagreed with the auditor’s assessment in the fall of 2021 regarding the “severity” of the problem.

The data obtained by POGO provides more details on mass close-outs of flags shortly before the second round of the program in mid-January 2021, further fueling concerns that they were not adequately reviewed. Businesses with uncleared flags were unable to access second-round PPP funds.

The end date for nearly 1.8 million, or 41.6%, of all the flags in the data is January 6, 2021 — far more than any other single day. The next most frequent end date is December 8, 2020, for 953,302, or 22.3%, of the flags. On the third most frequent end date, January 5, 2021, 6.7% of flags were closed. As of late September 2021, 97.4% of flags had been cleared over 289 days.

While it is possible that the SBA has applied new flags to loans since September 2021 — the date POGO obtained the dataset — the SBA approved the last PPP loans in May 2021. The SBA applied nearly 98% of its flags between August 2020 and December 2020, then swept away the vast majority of them within the first weeks of 2021.

The auditor’s findings show that the federal government did not conduct adequate due diligence before clearing tens of billions of dollars in collective debt owed by PPP recipients. Some of these recipients are companies owned by wealthy individuals or others where there is evidence they did not need PPP loans. POGO has previously reported on millions of dollars that flowed to a Ukrainian billionaire’s U.S. companies and substantial loans to candidates for political office who made massive donations to their own campaigns in 2020 shortly after their companies received the federal dollars.

The SBA says it is committed to a thorough review of PPP loans. An SBA spokesperson said that the Biden administration has an effort that utilizes both “automated technology that flags high-risk loans for further analysis” and manual reviews of “randomly selected loans on an ongoing basis.”

“When complete, 144,000 loans totaling $50 billion will have been closely reviewed for potential fraudulent activity, PPP loan eligibility, and compliance with forgiveness requirements,” emailed an SBA spokesperson.

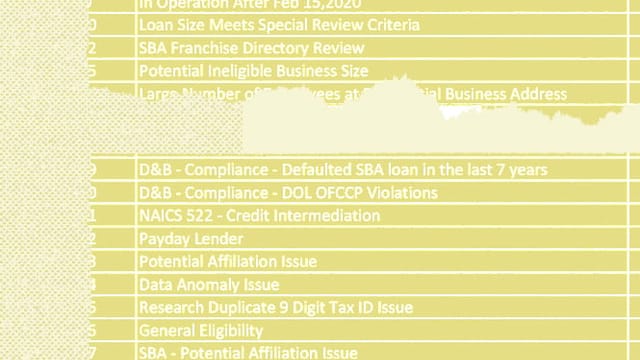

57 Varieties of Flags

A flagged PPP loan does not necessarily mean there was fraud, but some flags — if accurate — indicate clear-cut reasons a recipient would have been ineligible for the taxpayer-backed loan.

One flag associated with 785,089 loans indicates the recipient businesses did not exist prior to February 15, 2020, and therefore were not eligible to receive loans.

It’s the most common of the 57 different flags in the database. The SBA redacted 13 hold code descriptions under Freedom of Information Act exemptions that protect internal deliberations and information compiled for law enforcement purposes.

The SBA did not provide POGO with loan recipient names, but did provide the counties and states where the recipients are located. The government also provided POGO with loan amounts in ranges to make it more difficult to identify recipients. Over 70% of the flagged loans (1.65 million) were for $50,000 and under. Roughly 2% of the flagged loans (54,000) were for over $1 million.

However, POGO was able to identify potential matches for some of the flagged loans.

For instance, the Greenbrier Hotel Corporation in Greenbrier County, West Virginia — which is owned by West Virginia Governor Jim C. Justice II and his family — received an $8.9 million PPP loan that the SBA completely forgave in August 2021. It appears to match a loan in that county that the SBA flagged eight times. Justice’s other companies received five additional PPP loans, worth $6.3 million in total.

Many of the flags were for the company’s potential affiliations with other entities, as well as for potentially exceeding the eligible size to qualify for the PPP loan, among other reasons.

Recently considered the richest man in West Virginia, Justice was a billionaire when he was elected governor in 2016, but, as of last year, Forbes magazine estimated that his net worth runs north of $400 million. The Greenbrier’s occupancy was adversely impacted during the pandemic in 2020. Neither the Greenbrier, nor any of the other Justice-owned companies that received PPP loans, has been accused of fraudulently obtaining PPP loans. An attorney representing the Greenbrier had no comment and an SBA spokesperson would not comment on individual borrowers.

The largest PPP loans each had at least one flag simply by virtue of their size, not necessarily because there was anything suspicious. The SBA and Treasury Department announced a policy in 2020 that it would review every loan above $2 million.

Some 13,132 loans above $2 million only have that one flag for “Loan Size Meets Special Review Criteria.” An additional 15,605 loans above that amount have that flag and at least one more.

On January 16, 2021, the SBA cleared out 99.1% of all flags issued on this basis. The SBA cleared the other 0.9% during the preceding months. The bulk closure of most of these flags on one day suggests that not all of these large loans received the “full review” that then-Treasury Secretary Steven Mnuchin pledged they would get.

An SBA spokesperson did not comment on the bulk close-out of these flags in January 2021 during the Trump administration, but said that, under Biden's SBA leadership, the agency is looking at “more than 10,000 loans of $2 million or more totaling $33 billion, representing over one third of the total loans over $2 million. ”

Large recipients could come under scrutiny for other reasons too. Generally, if companies had more than 500 employees or exceeded another SBA standard, then they were supposed to be ineligible for PPP loans. Some 4,144 PPP loan recipients were flagged for “Potential Ineligible Business Size.”

Hot Spots

One loan worth between $2 million and $5 million to a recipient in Dallas County, Texas, received 13 flags — the most of any in the data.

Two hundred seventy loans each had nine flags or more. On the other end of the spectrum, 1.2 million loans received one flag each.

Some loans have more than one flag for redundant reasons. As in the Greenbrier example, some companies have multiple hold codes indicating that the recipient might be affiliated with other companies. Under certain conditions, affiliations between companies can render them ineligible if their combined size exceeds the SBA’s standards for eligibility.

For instance, the recipient of an over-$5 million loan in Kenton County, Kentucky, flagged nine times for potential eligibility issues, appears to be Columbia Sussex Corporation, which according to a local news report owns or operates more than 50 hotels in 22 states and has $850 million in annual revenue (currently, the company’s website lists 41 hotels in 18 states). Columbia Sussex-owned or operated entities received other PPP loans worth $49.6 million, according to SBA data. Neither the Columbia Sussex Corporation nor any affiliated entities have been accused by the Justice Department of PPP fraud. Columbia Sussex did not respond to a request for comment and an SBA spokesperson would not comment on individual borrowers.

Normally, such affiliations would render an applicant for an SBA loan ineligible because the collective size of these entities makes them larger than the SBA’s definition of a small business.

According to the Pandemic Response Accountability Committee, some fraud schemes that have already led to prosecutions “involved circumventing affiliation rules.” The committee wrote that “applicants could submit their parent company information to one or more lenders and their subsidiary company information to one or more lenders to appear as independent entities, although they are not. This was done in order to obtain multiple loans.” Also, if during the loan application process, an “applicant checked the affiliation box ‘No’ on the PPP application, there was no further review.”

However, Congress granted hotel and restaurant chains a controversial exemption in the law creating the program, enabling each separate hotel and restaurant in a chain to apply for PPP loans. But other reasons could render such loan applicants ineligible.

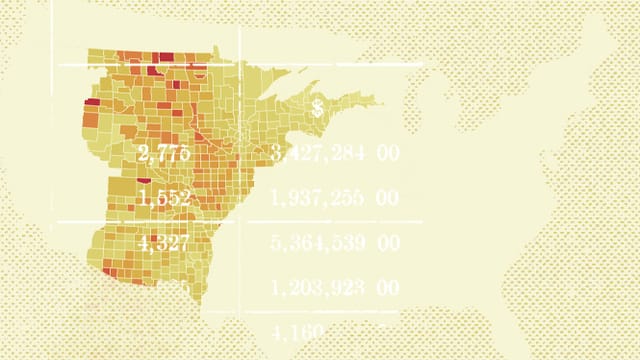

The largest states have the most businesses with flagged loans: California, Texas, Florida, and New York. An unusually large number of loans with flags compared to its population are in Puerto Rico.

Using census data on the number of businesses in each county in 2020, POGO identified the counties with the most flagged loans adjusted for the number of businesses. In absolute numbers, Los Angeles County has the most flagged loans, but adjusted for the size of its business community, it falls toward the middle of over 3,000 counties.

Hot Spots: Midwest, Puerto Rico Counties Among Those with Most Flagged Loans Per Business

According to POGO’s analysis of the data, 12 of the 15 counties with the most flagged loans per business are in Puerto Rico (seven counties) and North Dakota (five counties). Most of these are sparsely populated counties where a relative handful of flagged loans are all that’s needed to catapult the county to the top of the list. The notable exception is Guaynabo in the San Juan, Puerto Rico, metropolitan area, with 2,375 flagged loans and 2,188 business establishments in 2020.

Amplifying Structural Racism

The third most common flag — used 553,997 times — is associated with a policy initially issued by the Trump administration. The policy originally barred access to PPP loans by businesses owned by individuals with pending criminal charges regardless of whether they were misdemeanors or felonies, those serving parole or on probation, or persons who had been convicted of a felony of any kind within the last five years. The SBA would not comment on how the Trump administration used the flag, which denoted a possible match between a PPP loan recipient and a criminal record. SBA applied these and other flags after loans were approved.

Critics argued that the policy was overly broad and amounted to exacerbating the impacts of racial disparities in the criminal justice system. They argued that this also undermined the program’s aims because it locked out numerous business owners and their employees from receiving assistance. RAND Corporation researchers found this policy “differentially affected Black individuals,” estimating that 24% of affected businesses were Black-owned.

“The criminal justice system already disproportionately impacts people of color, and destructive policies that create unnecessary barriers to much-needed resources — such as the PPP — serve only to amplify the structural racism in our justice system,” said Andrew Glazier, president and CEO of Defy Ventures, a nonprofit that helps formerly incarcerated people learn business skills, in a statement in 2020.

A federal court struck down that policy as unlawful in response to a lawsuit by Defy Ventures and other plaintiffs. The Trump administration scaled back the policy’s scope to focus on felonies related to fraud, bribery, embezzlement, and false statements related to loan applications or financial assistance. The Biden administration further narrowed it in early 2021. As a result of those changes, many small businesses first locked out of the program later became eligible. But the data obtained by POGO shows that many people who received loans were still flagged because of data matches associating them with criminal charges.

Although SBA’s short-lived original policy barred businesses owned by people criminally accused — but not convicted — of offenses unrelated to fraud, the SBA never blocked access to PPP loans to people or companies who paid significant settlements to resolve civil claims of fraud, even allegations of defrauding federal small business programs.

The original PPP rules overlaid on top of an unequal justice system amounted to further penalizing those who already faced criminal accountability, and even penalized those who were only facing allegations of wrongdoing but who had not been convicted.

RAND estimated that the original PPP rules affected 31,620 Black-owned businesses. As a point of comparison, RAND estimated that 93,640 white-owned businesses were also affected. While that number is nearly three times larger, the white population in the U.S. is roughly five times more than the Black population, which is why RAND found the policy had disparate but not exclusive impact on Black-owned businesses.

After the rules were substantially changed, the RAND Corporation estimated that most affected businesses — employing more than 325,000 people — became eligible for PPP funds. “The impact was particularly large in the retail, construction, waste management, and manufacturing sectors — sectors that historically include high numbers of people with criminal history records,” RAND found.

Allegedly Dead or Debarred

Even setting those criminal record flags aside, there is still a large universe of questionable Paycheck Protection Program loans that merit closer scrutiny by resource-strapped federal watchdogs — even as most PPP loans have already been forgiven by the SBA.

And, although they represent a tiny fraction of the flagged loans in the database, many have already led to federal indictments. One example is a Riverside County, California, recipient of a loan exceeding $5 million with 10 flags that appears to be Road Doctor California LLC. Its owner, Oumar Sissoko, was convicted in April 2022 for misappropriating some of the money.

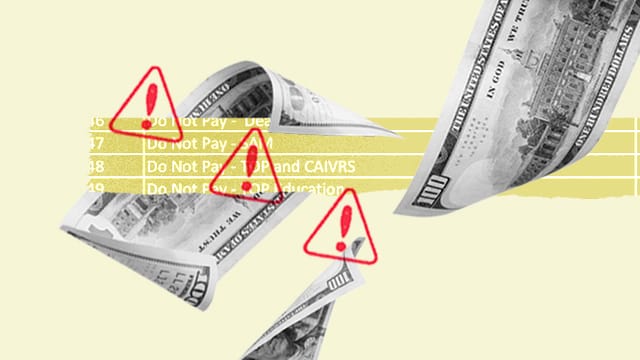

Another basis for denying PPP loans is appearing on the federal government’s list of entities that have been debarred from winning contracts, grants, or loans. A broader dataset managed by the Treasury Department is called the “Do Not Pay” list. It contains information on debarred entities, plus data on dead persons and borrowers with delinquent or defaulted federal loans.

The SBA data shows that 4,663 loans were flagged with “Do Not Pay — Death Sources.” One example is the previously mentioned loan worth between $2 million and $5 million to a recipient in Dallas County, Texas, that received 13 flags, including the death source flag.

Other loans with numerous flags, such as loans each worth between $1 million and $2 million in New Castle County, Delaware, and Los Angeles County, California, were also flagged because the recipient’s reported owner is a potentially dead person, along with six other reasons.

The SBA flagged 926 loans as “Do Not Pay — SAM.” SAM is a reference to a federal database of companies and persons excluded from doing business with the government.

Two recipients in Oakland County, Michigan, of two large loans — one worth more than $5 million and another worth between $2 million and $5 million — were flagged as appearing as entities in the federal SAM database. Those recipients were each flagged for four other reasons.

False positives could mean these or any other flags were wrongly attributed to PPP loan recipients. In any case, the flags for potentially matching dead persons or excluded entities came months after most PPP loans had already been made.

In January 2021, the SBA’s office of inspector general published a management alert — an urgent warning to the agency due to a serious issue that cannot wait for the results of a typically lengthy review. That alert said that some $3.6 billion in PPP loans went to recipients on the Treasury’s Do Not Pay list. Before going public, the watchdog first warned SBA privately on November 30, 2020. “This issue requires immediate attention and action,” according to the watchdog report. “Treasury’s analysis of potentially ineligible recipients demonstrates the importance of front-end controls and careful review by SBA of the loans identified.”

The head of the SBA at the time, Jovita Carranza, defended her agency’s performance. “Prior to the Management Alert, SBA developed systems to screen potential borrowers against the Treasury Department’s Do Not Pay List,” she wrote, without mentioning when SBA’s effort began. According to the SBA data obtained by POGO, the SBA’s effort only preceded the watchdog’s warning by weeks. The data shows that November 1, 2020, marks the first day PPP loans were flagged for matches with the Do Not Pay list — seven months after the first PPP loans were approved in early April 2020.

Most PPP funds had been distributed in the program’s first months, meaning the vast majority of PPP recipients never faced screening against the Do Not Pay list before they were lent PPP funds. Given that the SBA also failed to ensure the adequacy of the back-end review of loan forgiveness applications, it’s unclear if many of the loan recipients that are on the Do Not Pay list received the scrutiny they deserved at any point.

Signs of Implausible Businesses

The push to move PPP loans out the door as quickly as possible was motivated by an effort to protect millions of jobs. But significant sums appear to have been diverted to entities that may not be real businesses, may not have been in operation when PPP loans were sought, or could not have realistically employed the number of workers claimed.

SBA flagged 239,144 loan recipients as having an “inactive business.” One example is a loan worth between $1 million and $2 million that went to a recipient in Ulster County, New York, that had been flagged for nine other reasons. Twenty-six other recipients flagged for having an inactive business address also had 10 flags or more.

SBA flagged 48,427 loans because of data matches showing the recipients’ business addresses as “currently vacant.” One example is in Austin, Texas, where a loan between $350,000 and $1 million was flagged for this reason, as well as eight others.

The SBA flagged 5,811 loans because its analysis identified a large number of employees at the residential addresses provided by the PPP recipients as their place of business.

Working from Home? PPP Recipients Flagged for Having a Large Number of Employees at a Residential Address

A loan worth between $2 million and $5 million to a recipient in Cumberland County, Pennsylvania, was flagged for having many reported workers at a residential business address (and for nine other reasons).

Using publicly available data, researchers at the University of Texas engaged in a similar effort as the SBA, including finding PPP recipients at residential addresses. Some of these loans had signs of potential fraud, such as numerous loans flowing to different businesses at the same address.

“As an example, a modest suburban home north of Chicago with an estimated home value of $170 thousand per Zillow received 14 loans at a single address, all with colorful business names, almost all in the same industry, most with the same loan amount, and all backing ten jobs,” according to the University of Texas study.

PPP Recipients that Laid Off Workers

Even though the purpose of the Paycheck Protection Program was to keep workers on the payrolls of businesses, some PPP loan recipients laid off employees. Businesses with 100 or more employees are legally required to send notices to employees in advance of layoffs of 50 or more under the Worker Adjustment and Retraining Notification (WARN) Act.

The SBA flagged 388 businesses for issuing COVID-related WARN notices.

A loan worth more than $5 million to a recipient in Clark County, Nevada, was flagged for issuing a WARN notice.

Out of the 388 loans flagged for this reason, a disproportionate number — 306 — went to entities in New York state. This raises questions about whether the SBA was consistent in its assessment across the nation of recipients’ compliance with the terms of the PPP loans, which were intended to preserve jobs, or if there is some other explanation such as the fact that New York state was the nation’s pandemic epicenter when the PPP began. An SBA spokesperson had no comment.

The 388 loan recipients flagged by the SBA is far smaller than the number identified by the nonprofit, pro-union organization Good Jobs First. In a December 2020 report, Good Jobs First “conservatively” identified 1,892 companies that received PPP loans that also sent layoff notices affecting over 190,000 workers earlier that year.

One reason the SBA may have flagged far fewer PPP recipients than Good Jobs First is that two-thirds of the layoffs identified by the nonprofit came in the month before the SBA lent out the first PPP loans.

Front-End Oversight in Short Supply

Earlier this year, SBA Inspector General Hannibal “Mike” Ware issued a report on the agency’s systematic failure to tackle fraud until nearly two years after the PPP was launched in the spring of 2020.

Part of the problem was responsibility for fraud was diffuse within the SBA. “SBA did not have an organizational structure with clearly defined roles, responsibilities, and processes to manage and handle potentially fraudulent PPP loans,” according to Ware’s May 2022 report. And it wasn’t until the end of this February that SBA created “a centralized entity to design, lead, and manage fraud risk.”

That nearly two-year delay had consequences.

No one was in charge of an anti-fraud effort at the SBA.

From the start, banks and other lenders sought detailed guidance from the SBA on how to deal with applicants they believed might be fraudulently seeking loans or were otherwise ineligible. The SBA told its watchdog that existing industry regulations could have filled this role. But the inspector general was not convinced. “These gaps weakened SBA’s ability to actively reduce and combat fraud and increased the risk of fraudulent and ineligible applicants receiving PPP loans and loan forgiveness,” the inspector general wrote.

The watchdog even published a white paper examining past loan programs on the day the PPP began distributing loans. It warned that allowing loan applicants to self-certify their information without supplying sufficient back-up documentation has resulted in inappropriate or unsupported loan approvals. Ware urged the SBA to put proper controls in place before disbursing funds.

These oversight shortfalls would have been bad under normal circumstances. But the consequences were exponentially greater in spring 2020 during the height of the rapidly spreading COVID-19 pandemic and with unemployment levels skyrocketing. From early April to early May 2020, the SBA lent out an amount worth more than 20 times what it had lent out in any single year. As the inspector general wrote that year, “increased loan volume, loan amounts, and expedited loan processing timeframes may make it more difficult for SBA to identify red flags in loan applications.”

One financial insider previously told POGO that his financial technology, or “fintech,” company, which processed PPP loans, had a skeletal anti-fraud effort during the first months of the program. The insider said that the fees paid to lenders for processing federal loans — where none of the lenders’ money was on the line — created a profit motive to look the other way when it came to signs of potential fraud or ineligibility.

This, coupled with a heavy reliance on what loan applicants claimed without any verification, created a “huge moral hazard,” the insider said. One partial solution would be using tax filings submitted to the IRS to confirm applicants’ claims. Even if the SBA decided to forgo this step during the chaos of spring 2020 to speed up the issuance of loans, the SBA could have sought consent from PPP recipients to access these IRS records during the PPP loan forgiveness process. But it has not.

In lieu of detailed guidance and using tax records to independently verify applicants’ claims, lenders, whether traditional banks or fintechs, varied in their due diligence practices before approving PPP loans. And even when one lender identified a potentially fraudulent loan application, the SBA did not “share potentially fraudulent applicants in real-time across lenders as an early warning system of possible sources or patterns of larger fraud schemes,” the Pandemic Response Accountability Committee noted in a report earlier this year. This led to “instances of applicants’ ‘shopping’ for weaker internal controls among lenders.”

One fintech lender has been drawing scrutiny from government watchdogs. Citing “a December 2021 fraud risk assessment conducted by the SBA’s contractor,” the Pandemic Response Accountability Committee wrote that “Kabbage — a Fintech business lender — processed more fraudulent loans and was second only after Bank of America in approving loans.” Justice Department filings first reported by the Miami Herald show that at least two U.S. attorneys’ offices are investigating Kabbage. Kabbage, which has recently filed for bankruptcy, did not respond to a request for comment.

No one was in charge of an anti-fraud effort at the SBA. Lenders grasped for guidance, with financial incentives to process loans without their own skin in the game. And it was a system that relied on applicants’ representations of their eligibility. It was a perfect storm for abuse. And this perfect storm involved an unprecedented volume and amount of federal loans issued in a very short period.

Watchdogs Under Water

The Small Business Administration office of the inspector general is a leading watchdog examining questionable PPP loans. The office received a tidal wave of complaints through its hotline. In the first year after the start of the program, the SBA watchdog office received “a 19,500% increase over prior years,” according to a congressional memo. SBA Inspector General Ware recently told the New York Times that he has limited the number of cases each of his agents can work at any one time to avoid burnout. On CNN, Ware has said his office is in possession of over 40,000 actionable complaints that could amount to a century’s worth of investigative work.

Earlier this year, Biden directed the creation of a lead prosecutor for pandemic fraud, who told the Times he expects law enforcement to work on PPP loan fraud cases for the next decade. Last month, Biden signed a law extending the statute of limitations for all PPP fraud from the standard five years to 10 years, giving watchdogs more time to work on the massive number of cases before them. “My message to those cheats out there is this: You can’t hide. We’re going to find you. We’re going to make you pay back what you stole and hold you accountable under the law,” Biden said.

In a press release on the new law, the bipartisan leadership of the House Small Business Committee, which introduced the bill, cited the disproportionate role of fintech lenders in PPP fraud cases as the basis for extending the statute of limitations. In early October 2020, POGO and Bloomberg News were the first to report findings on the higher rate of PPP fraud connected to fintechs — findings further confirmed by a recent University of Texas study.

Bank-originated loan fraud has a 10-year statute of limitations, but many fintechs are not considered banks. Thus, fintech-originated PPP loan fraud had a five-year statute of limitations until Biden signed the new bill into law.

Legal experts believe much of the fraud will be difficult to successfully prosecute criminally. One reason is applicants that may not have needed PPP funds only had to certify in good faith that “current economic uncertainty makes this loan request necessary.” Civil enforcement, including False Claims Act lawsuits brought by whistleblowers, may be more promising in these cases because there is a less daunting burden of proof. Last year, senators introduced bipartisan legislation to beef up civil and administrative enforcement. These bills have yet to become law.

“In light of the trillions of dollars that Congress has appropriated recently for COVID relief, these bills are needed, more than ever, to fight the significant amounts of fraud that we are already seeing,” Senator Chuck Grassley (R-IA) said in a statement last year.

The Fire Hose Approach

The federal response to COVID-19 in the spring of 2020 was chaotic on many levels. Given the challenges of that moment, it has been argued that the Paycheck Protection Program was a success because it — along with other federal relief efforts — offered a lifeline when the economy was in freefall. The speed of the program is viewed as a feature, not a bug. The SBA launched the program in early April 2020, just days after Congress authorized it in late March.

The argument is that, had the SBA taken weeks to set up the bureaucratic infrastructure to better target loans and prevent fraud before lending the funds, the economy would have further suffered. “There is a trade-off between efficiency, inclusiveness, and potential fraud,” said Bharat Ramamurti, a former member of the COVID-19 Congressional Oversight Commission and deputy director of the Biden White House’s National Economic Council, on a 2020 podcast.

The U.S. government’s failure to have systems in place ahead of time, unlike other nations, came at an enormous cost.

It is true that speed and inclusiveness were more important at that moment. Even with the quick launch, there were problems that impeded some businesses’ access to PPP loans — many of them Black-owned businesses. One study on the PPP shows that these early program stumbles had an adverse impact on employment, even if those affected companies eventually received the funds they sought.

But the U.S. government’s failure to have systems in place ahead of time, unlike other nations, came at an enormous cost. The SBA could have leveraged technology to ensure more robust front-end oversight far earlier than it did, as experts told NBC News earlier this year. The agency did not need to wait until early 2022 to set up a centralized fraud group. Nor did the SBA need to wait months before taking other key steps.

The Trump administration’s Office of Management and Budget also issued guidance that defied the law. That guidance ignored a legal requirement that stated that recipients of PPP loans above $150,000 had to report quarterly on what the money was used for, the jobs saved, sub-awards or payments, and so on. The spotlight of repeated reporting on how PPP funds were used could have been a deterrent to some fraudsters and might have provided an important detection tool for those looking into fraud. The Biden administration has not reversed course. Sources have told POGO that the Biden administration believed it was too late to start requiring these reports since most of the outlaid pandemic assistance — PPP loans included — had been used by recipients well before Biden became president and collecting backward-looking data at this point would be too burdensome and unreliable.

While it does not address fraud in any detail, a peer-reviewed paper by Massachusetts Institute of Technology Economics Professor David Autor and others, including Federal Reserve economists, offers a detailed assessment of the PPP’s first two tranches of loans. SBA dispersed its first two tranches of PPP loans between April and August 2020, which correspond to the vast majority of the flagged loans in the SBA data obtained by POGO (the third tranche allowed recipients of earlier PPP loans to get a second loan). The paper estimated that only between 23% and 34% of Paycheck Protection Program dollars “supported jobs that would otherwise have been lost.” The rest — 66% to 77% — “accrued to owners of business and corporate stakeholders.” About three-quarters of PPP funds went to the richest 20% of households by income. While the PPP did likely help boost employment in 2020, it did so “at a substantial cost of $169,000 to $258,000 per job-year saved,” the paper states. The PPP may have helped stave off some temporary business closures at the time, but it is not clear if it reduced the incidence of businesses closing for good.

Compared to stimulus checks and enhanced unemployment benefits, the paper found that “PPP was likely the least effective of the three programs in boosting the macroeconomy.”

“Ironically, the program feature that arguably made the Paycheck Protection Program’s meteoric scale-up possible is also the feature that made it potentially the most problematic: the program was essentially untargeted,” states the paper, which notes that business size was one of the few program limits.

But it didn’t happen this way in other nations.

“Targeted business support systems were feasible and rapidly scalable in other high-income countries because administrative systems for monitoring worker hours and topping up paychecks were already in place prior to the pandemic,” the paper states. “Lacking such systems, the United States chose to administer emergency aid using a fire hose rather than a fire extinguisher, with the predictable consequence that virtually the entire small business sector was doused with money.”

Having systems in place to ensure applicants are who they say they are and that their needs are legitimate would also tamp down fraud.

The Next Time

It is only a matter of time before other disasters strike. Spiking inflation and economic shocks from Russia’s invasion of Ukraine are the latest reasons showing why the U.S. government can never rest on its financial laurels.

There may be little to no advance warning before the next disaster, meaning any rapid response will have to make do with the systems in place. Even though Congress can rapidly pass laws and appropriate massive amounts of funding when it wants to — as it did during the spring of 2020 — it takes time to hire personnel, create administrative capacity, and craft thoughtful plans.

We know that big trouble is coming down the pike. Climate change is occurring at a rapid pace, and is already exacerbating extreme weather events. An overwhelming array of evidence points to the impacts only becoming worse in the years and decades to come.

There may be little to no advance warning before the next disaster, meaning any rapid response will have to make do with the systems in place.

The U.S. has long been able to absorb the economic impacts of localized disasters because it is a large, wealthy country. But we are in a new normal. There is more than enough evidence that the coming shocks will likely be larger, less localized, more numerous — and more expensive. Better preparation is needed.

A significant amount of front-end transparency can be a powerful way to ensure money goes where it is needed. During the Great Recession, the Recovery Act harnessed openness, and stimulus funding-related fraud was historically low. Unfortunately, media organizations and groups like POGO had to fight for transparency after the much larger amount of pandemic relief funding had already gone out the door in 2020.

The added irony is that Congress mirrored key aspects of Recovery Act oversight in the Coronavirus Aid, Relief, and Economic Security (CARES) Act. But the Office of Management and Budget ignored the CARES Act’s recipient reporting language. Furthermore, funding for the Pandemic Response Accountability Committee and that of offices of inspectors general was not commensurate with the increased spending they were overseeing. And agencies neglected to implement even basic fraud prevention in the service of speed above all else.

As the federal government chases down instances of PPP fraud, strengthening laws such as the False Claims Act that enable the federal government to recover funds and give watchdogs like the SBA’s inspector general’s office the resources it needs will help bring about accountability. But much of this waste, fraud, and abuse could have been stopped or at least spotted earlier. The millions of flagged PPP loans worth billions of dollars, and the lack of scrutiny leading up to their forgiveness, shows the great pandemic swindle was aided and abetted by the SBA’s lax oversight.